The bond spread is the differential in bond yields between two countries.

These distinctions give birth to carry trading, which we explored previously.

You may predict the direction of currency pairs by keeping an eye on bond spreads and interest rate forecasts.

This is what we mean:

The currency of the country with the higher bond yield rises versus the currency of the country with the lower bond yield as the bond spread between the two countries increases.

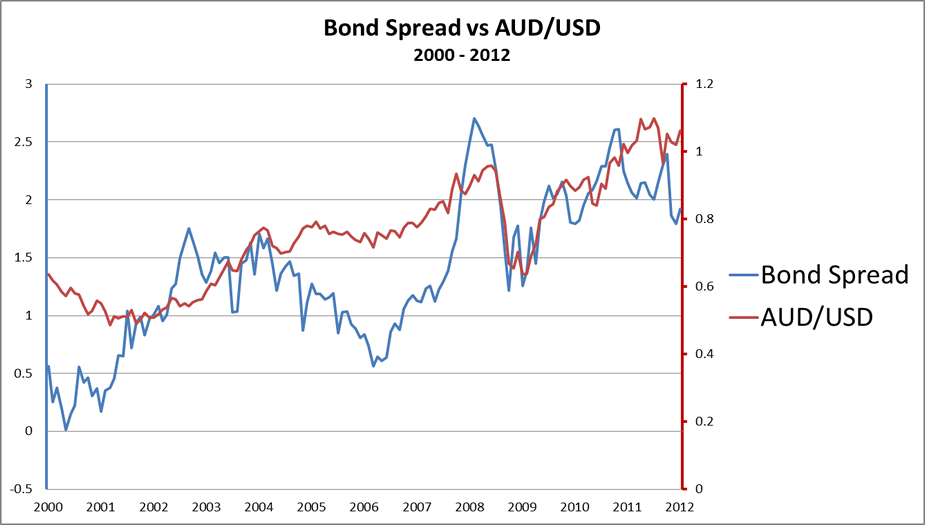

This tendency may be seen by examining the graph of the AUD/USD price action and the bond spread between Australian and US 10-year government bonds from January 2000 to January 2012.

From 2002 to 2004, as the bond spread increased from 0.50% to 1.00%, the AUD/USD increased by over 50%, jumping from.5000 to 0.7000.

When the bond gap increased from 1.00% to 2.50% in 2007, the AUD/USD increased from.7000 to just above.9000.

That’s 2000 pips!

When the 2008 crisis hit and all major central banks began to cut interest rates, the AUD/USD fell from the.9000 level to 0.7000.

So, what exactly happened here?

One possible explanation is that traders are taking advantage of carry transactions.

When bond spreads between Australian bonds and US Treasuries widened, traders increased their long AUD/USD positions.

WHY?

The GBP/USD fell as the bond spread between the UK bond and the US bond narrowed.